Part & Part Mortgage

Part & part mortgages are the least common form of repayment method, however, they are also the most flexible. They are designed to be a middle-point between repayment and interest only amalgamating the advantages of both repayment types whilst minimising the disadvantages.

Part & part mortgages are the least common form of repayment method, however, they are also the most flexible. They are designed to be a middle-point between repayment and interest only amalgamating the advantages of both repayment types whilst minimising the disadvantages.

What is a Part & Part mortgage?

A part & part mortgage is simply a mixture of capital & interest and interest only. You choose the amount of your mortgage you would like to be on interest only and the amount to be on capital and interest.

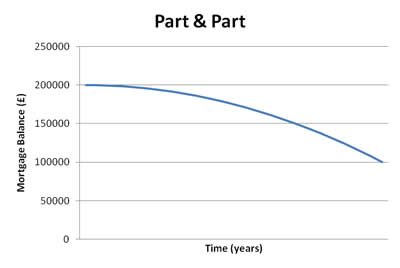

Let's say you have a £200,000 mortgage and will retire in 25 years. On retirement, you know your pension will provide a lump sum of £100,000. One of your choices could be to opt for a part and part mortgage where £100,000 is on repayment and the other £100,000 is on interest only which would reduce your monthly repayments. The graph below shows how the £100,000 repayment portion slowly reduces leaving the £100,000 interest only portion remaining at the end. This would then be paid off from the pension lump sum.

A graph illustration how a £200,000 part & part mortgage would be repaid over time with £100,000 on capital & interest and £100,000 on interest only

Part & part mortgages can be used with any situation where you are expecting a windfall such as an inheritance, an investment policy maturing, a work bonus or even if you feel you have a lucky lottery ticket (although it's not recommended you structure your mortgage around this!).

In the long term, a part & part mortgage works out more expensive than a repayment mortgage but cheaper than an interest only mortgage. The table below shows how a 25-year part & part mortgage of £100,000 interest only and £100 repayment compares to comparable fully interest only and fully repayment mortgages.

Like the other repayment types, you can switch to a full repayment or full interest only mortgage in the future. You can even change the split between both portions on your part and part mortgage. Your lender may charge a small fee for doing so.

| Repayment Mortgage | Interest Only Mortgage | Part & Part Mortgage | |

| Original amount | £200,000 | £200,000 | £200,000 |

| Monthly repayment | £1,366.35 | £1,083.33 | £1,224.83 |

| Total repayments | £409,905 | £325,000 | £367,450 |

| Balance after 25 years | £0 | £200,000 | £100,000 |

| Total amount payable | £409,905 | £525,000 | £467,450 |

Advantages of Part & Part mortgages

- Part & part mortgages give you the ability to take advantage of the features of both interest only and repayment mortgages

- The monthly repayments will be cheaper than a comparable capital & interest mortgage due to the interest only element

- In the long run, part & part mortgages are cheaper than fully interest only mortgages as part of the capital is repaid

Disadvantages of Part & Part mortgages

- The monthly repayments will be more expensive than a comparable interest only mortgage due to the capital repayment element

- In the long run, part & part mortgages are more expensive than fully repayment mortgages due to the interest only part so the capital remains at the end of the term

Summary

- Part & part mortgages are a mixture of repayment and interest only

- You can choose the amounts on each repayment type

- You can amend the amounts at any time or even switch to a full repayment or full interest only mortgage

For more information about 'Part And Part Mortgages', you can call us on 020 8783 1337 or submit an online quote.

Bookmark with: