Fixed Rate Mortgage

Fixed rate mortgages are one of the most popular choices of mortgage product within the mortgage industry (both in the UK and USA) mainly because of the certainty of repayments they provide therefore allowing you to budget your finances.

What is a Fixed Rate Mortgage

A fixed rate mortgage, as the name implies, is one that offers a fixed repayment amount for a specific period of time (typically 2,3 or 5 years although much longer periods are available). The interest rate is fixed at the start of the product by the mortgage provider and they will guarantee that same interest rate until the product expires. After the agreed period, the interest rate owed on the loan usually reverts to the lender's standard variable rate.

Typically, the longer the period of fixed rate, the higher the fixed interest rate will be as the mortgage provider is taking a greater risk, however, this is not always the case as it also depends of market conditions and how aggressively each mortgage provider is pursuing fixed rate mortgage business.

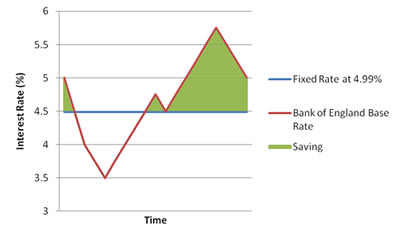

Example of the savings with a fixed rate mortgage against variable rates.

If you wanted to exit the product before the agreed term, an early redemption charge is usually applicable and generally quite significant. For example, you may be charged six months gross interest if you leave a five-year fixed rate agreement before the expiry date. Most lenders use percentages for their early redemption charges so a charge of 2% would mean you will be charged 2% of the outstanding mortgage balance should you redeem the mortgage within the fixed rate period. There are also stepped redemption charges and you may see a 5-year fixed rate mortgage with a redemption charge of '5/4/3/3/3'. This means that in Year 1, you would be charged 5% of the outstanding mortgage balance, 4% in Year 2 and 3% in Years 3-5.

Some redemption charges could even go beyond the fixed-rate period. This would be an 'overhanging redemption penalty'. Always read the mortgage offer carefully as you must be clear on what everything means.

Some mortgage lenders allow you to overpay your fixed rate mortgage up to a specific amount without incurring any early redemption charge. Should you overpay beyond this limit, you are usually charged the early redemption charge on the amount overpaid beyond this limit. e.g. If you are permitted to overpay £15,000 in any one year and your early redemption charge was set at 2%, this would mean that in the event you overpaid the mortgage by £25,000, you would be charged a redemption fee of £200. (£25,000 - £15,000 = £10,000; £10,000 x 2% = £200).

Advantages of Fixed Rate Mortgages

- Fixed rate mortgages ensure that your mortgage repayments will remain at a certain amount for the duration of the product.

- As your repayments are a fixed amount, this allows you to budget for your mortgage repayments so you can better manage your finances.

- Should interest rates increase during the term of the product, you will have peace of mind that your mortgage payments will not increase.

- Some fixed rate mortgages allow for overpayments up to a specified amount.

Disadvantages of Fixed Rate Mortgages

- You are generally committed to a fixed rate mortgage as they generally carry an early redemption charge should you want to come out of the product early.

- Fixed rate mortgages usually carry a slightly higher interest rate than their variable rate equivalents due to the interest rate risk.

- Should interest rates decrease during the fixed rate product, your mortgage repayment will remain at the same fixed amount and so you will not see any benefit.

Advice when choosing a fixed rate mortgage

- Read the mortgage offer carefully. Some providers offer a lower fixed interest rate in exchange for a longer early redemption charge period. For example, if you chose a 2-year fixed rate which carried a 3-year early redemption charge, this would mean that after your fixed interest rate of 2 years is over, you would be committed to the lenders' standard variable rate for another year (which is typically higher than variable rate products).

- If you are considering moving home within the fixed rate period, check that the mortgage product is portable (i.e. it allows you to transfer the fixed rate to the new property). This will avoid the need to pay the early redemption charge and most lenders will generally charge only a nominal 'porting fee' for doing so.

- If you are able to overpay your mortgage, check the amount you are permitted to overpay each year meets your requirements. Most will allow you to overpay either a specified amount or a certain percentage of the outstanding mortgage balance.

For more information about 'Fixed Rate Mortgages', you can call us on 020 8783 1337 or submit an online quote.

Bookmark with: